Policy Recommendations

- The EU should introduce a border carbon adjustment based on Article II(2) of the General Agreement on Tariffs and Trade (GATT) to complement the EU Emission Trading System.

- The Emission Trading System should be transformed into a quasi-carbon tax by introducing a narrow price corridor for the ‘European Emission Allowances’ price, of which the lower bound could be used as a tax rate for a border tax adjustment.

- Using the existing product-based benchmarks within the Emission Trading System as the basis of a border tax adjustment would make it comply with the Interpretative Note of Article III. of the GATT and would also allow for designing a full border tax adjustment, i.e. exempting EU exports to third countries from any form of carbon pricing.

Abstract

The European Commission has announced to step up carbon emission reduction targets for 2030 and 2050, respectively. These targets would require even bigger efforts to price carbon emissions at the EU as well as at the national level. The EU and its member states will find themselves in a position of increasing costs of production due to those efforts while other emitters such as China, acting within the Paris Agreement framework, will be allowed to increase their emissions until 2030. The United States are exiting from the Paris agreement altogether and are actively reducing environmental standards.

In this situation the calls for implementing a border carbon adjustment (BCA) to complement the EU Emission Trading System (ETS) are becoming louder. Most recently, the new von der Leyen European Commission in their just released plans for a European Green Deal announced to propose a BCA mechanism for the EU. In theory a BCA would be a perfect mechanism to enable unilateral carbon pricing avoiding a loss of competitiveness and the resulting carbon leakage vis-à-vis third countries. Implementation of an EU BCA, however, is not only politically contentious, but also rather complex from a legal perspective. This policy brief therefore focuses on issues of implementation.

****************************

How to implement a WTO-compatible full border carbon adjustment as an important part of the European Green Deal

Introduction

In a recent contribution, Jean Pisani-Ferry[1] (chief economic advisor of the French President Emmanuel Macron during his election campaign) addresses the fundamental problem of bringing in line the EU’s free trade agenda, one of the very few exclusive competences of the European Commission, and the EU’s ambition to lead the way in the field of climate protection. Effective unilateral climate action is already challenging under the current EU 2030/2050 goals, but the new push to agree to even more ambitious goals by the new von der Leyen Commission within the proposed European Green Deal has to solve the issue of carbon leakage first. The existence of carbon leakage[2], i.e. a global increase in carbon emissions as a consequence of unilateral climate action due to the shift of production to countries/regions with lower environmental standards, in all its forms[3], is a contentious issue because it is hard to determine empirically. For this reason, the question whether the EU’s carbon pricing mechanism, the EU Emission Trading System (ETS), was and is responsible for carbon leakage still remains to be answered. However, recent econometric studies like the one by Aichele and Felbermayr (2015), concluding that the Kyoto Protocol was indeed responsible for carbon leakage, as well as the standard economic insight that at least in the long-term production will move to regions with lower costs of production should be taken seriously. The problem of the EU is that the more ambitious carbon reduction targets are the quicker will the current ETS carbon leakage provisions run their course because the amount of ‘free’ European Emission Allowances (EUA) is reduced by the same annual reduction factor (at the moment 2,2% for the 4th trading period 2021-2030) as is the overall amount of EUA.

More ambitious 2030/2050 reduction targets would imply an even larger annual reduction factor and thus even higher EUA prices.

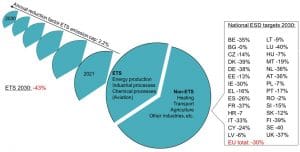

Graph 1: current EU carbon reduction path for the 4th trading period (2021-2030)

source: own

source: own

In theory, a border carbon adjustment mechanism, as proposed by the Commission in its Green Deal, would be the ideal instrument to safeguard EU industry.

Graph 1 depicts the EU’s overall emission reduction path till 2030. The 43% reduction in the ETS sectors and the 30% reduction in the non-ETS (Effort Sharing Decision) sectors are relative to the 2005 emissions, so that combined the reduction will amount to 40% compared to the base year 1990. At the moment the price for one allowance, i.e. the right to emit one ton of carbon, amounts to 25 €. Because of the Market Stability Reserve[4] (MSR) that finally deals with the oversupply of allowances and due to the increased annual reduction factor the price is likely to increase significantly in the 4th ETS trading period (2021-2030). More ambitious 2030/2050 reduction targets would imply an even larger annual reduction factor and thus even higher EUA prices.

Article 10a(5a) of the amended ETS directive 2003/87 gives some flexibility regarding the annual ratio of auctioned to ‘free’ (57:43) allowances but overall this ratio will remain fixed. Therefore, the amount of ‘free’ allowances, i.e. the protection against carbon leakage, will be reduced annually by a reduction factor of at least 2,2%. Combined with the fact that the United States formally notified the United Nations that they will withdraw from the Paris climate accord and that the same administration is continuously cutting back on environmental/emission standards, and considering that other big emitters of carbon are allowed to increase their carbon emissions until 2030, protecting European industry against carbon leakage should be at the top of the Commission’s agenda.

In theory, a border carbon adjustment mechanism, as proposed by the Commission in its Green Deal, would be the ideal instrument to safeguard EU industry. However, given the political reality and existing international trade law, designing a border carbon adjustment (BCA) in a way that the actual amount of greenhouse gases emitted in the production of imported goods can be priced adequately is a huge political and legal challenge. In the following we will discuss the relevant articles of the General Agreement on Tariffs and Trade (GATT) one by one in order to eventually derive one of the very few options available to legally implement in the foreseeable future an EU BCA by securing its WTO compatibility. This policy brief focusses on issues of implementation and can thus be understood as an add-on to the paper by Krenek et al. (2019). The aim here is not to outline an optimal BCA design but a design that actually can be implemented unilaterally within the existing framework of international trade law.

The aim here is not to outline an optimal border carbon adjustment (BCA) design but a design that actually can be implemented unilaterally within the existing framework of international trade law.

WTO compatibility of an EU BCA

When approaching this topic, it is useful to distinguish between the general rules that allow WTO member states and signatories of the GATT to introduce trade restricting measures on the one hand and exceptions to these rules on the other hand. The relevant general rules for the introduction of a BCA can be found in article I., II., III., XI. and XVI. of the GATT. The article that might allow a member state to deviate from these general rules in the case of implementing a BCA is Article XX.

Most favoured nation principle

It should be emphasised that a BCA design based on individual carbon footprints is not only doomed because of its impracticality.

Article I. of the GATT represents one of the two best known principles of the GATT, namely the “most favoured nation principle” (MFN principle). It states that a country is not allowed to discriminate between imported products from different countries and/or producers if the products in question are considered as “like” products, i.e. similar products. The debate of what constitutes the concept of “likeness” ultimately produced 4 guiding principles: i.) characteristics of the product, ii.) end use of the product, iii.) how the respective product is qualified in the schedule of concessions of member states, and iv.) consumers’ tastes and habits, i.e. whether a product is attracting the “same” consumers. Thus, ‘production method’ is not an established criterion to determine whether or not two products are “like” products. If, for example, two cars at the border of the EU are ‘like products’ according to the four criteria mentioned above, but differ in their carbon foot-prints as a result of different production methods, the EU is not allowed to discriminate between the two cars. Although there is important case law, e.g. US – Import Prohibition of Certain Shrimp and Shrimp Products (WT/DS58) that deals with requiring a specific production method for environmental reasons, its applicability for carbon footprints would not be easy even in the case of perfect information, i.e. knowing the exact carbon footprint of every product.

It should be emphasised that a BCA design based on individual carbon footprints is not only doomed because of its impracticality. It would establish ‘production method’ as the main criterion to discriminate between products in order to allow for different tax rates at the EU border for products identical in terms of characteristics, but produced, e.g., with a different carbon footprint. Such a radical approach of changing the MFN principle is not likely to succeed.

Pacta sunt servanda

Even if there is a theoretical BCA design that would somehow be admissible under article I. and even if there would be a universally accepted method to calculate the carbon footprint of imported products, article II. would quickly put an end to any attempts that propose an EU BCA design that tries to levy higher tariffs on relative “dirty” products, i.e. “like” products with a bigger carbon footprint.

Article II(1) simply states the principle of pacta sunt servanda, i.e. existing laws that include the national tariff schedules are to be respected. For most of the traded goods (classes of goods) there are already agreements regarding tariff rates. It would be possible to lower tariff rates unilaterally, implying that these reduced rates have to be granted to all WTO member states due to the MFN principle. Increasing tariff rates, however, is subject to negotiation and agreement between WTO members. Details on how the schedules can be changed can be found in article XXVIII.

The way forward

Article II(2), however, is one of the few pathways that would allow to introduce a specific WTO-compatible BCA design. “Nothing in this Article shall prevent any contracting party from imposing at any time on the importation of any product a charge equivalent to an internal tax imposed consistently with the provisions of paragraph 2 of Article III. in respect of the like domestic product or in respect of an article from which the imported product has been manufactured or produced in whole or in part; […]”

This angle of levying a tax or a tariff equivalent to the burden imposed on domestic producers, irrespective of the carbon content of the imported product, appears as the only viable pathway to introduce a WTO-compatible BCA[5]. This approach has two prerequisites, namely a transparent calculation of the tax (tariff) base and a transparent tax (tariff) rate. Both is not a trivial undertaking but most feasible when compared to other approaches. For the tax (tariff) base the existing benchmarks within the ETS, used for the allocation of free allowances, would be the basis to establish a so-called EU best-technology standard. These benchmarks are in most cases already product-based. Undoubtedly the calculation of these standards would have to undergo renewed scrutiny before becoming the basis of a BCA, but this can be achieved in the very short term.

The identification of an acceptable tax (tariff) rate is definitely the most difficult part of the reform. Most recently Kemfert et al. (2019), with regard to the current carbon pricing debate in Germany, emphasised the importance of a stable, predictable CO2 path (mainly) within the ETS. Firms have to know beforehand what additional costs they will face in the future in order to plan and make the necessary (technological) adjustments and investments. A strongly volatile EUA price will have a negative impact on the technological transition of EU industries to less carbon-intensive methods of production.

The identification of an acceptable tax (tariff) rate is definitely the most difficult part of the reform.

Thus, we suggest the introduction of a very narrow price corridor within the ETS of which at least the lower bound can be used as a tax (tariff) rate for imports.

National treatment principle

The second well-known principle is the “national treatment” principle, i.e. article III. of the GATT. This article is also based on the concept of “likeness”. GATT parties have agreed to not discriminate between imported products and domestically produced “like” products. This refers to domestic taxes and levies, but also regulations and implies that member states not only are not allowed to discriminate between two “like” imported products but they are also not allowed to discriminate between one imported product once it has entered the country and a “like” domestically produced product. Solving the problem through national tax schemes is therefore not an option if the regulator tries to tax the imported product differently than the domestic product by assuming a different carbon foot print. It would, however, be feasible to tax two “like” products, one produced in the EU and one outside the EU, with the same tax rate, i.e. irrespective of their carbon content. In this regard the Value Added Tax (VAT) is a good example how a future border tax adjustment could be put into practice.

With reference to the Working Party Report on Border Tax Adjustments[6] of 1970 the Interpretative Note of Article III[7] states that our proposed border tax is admissible under the condition that it is product-based. Thus, the usage of the product-based benchmarks of the ETS is crucial.

Unlikely success of integrating foreign producers into the ETS

Article XI. is relevant because it emphasises that among trade restrictions quantitative restrictions are to be avoided above all else. This means that every tariff is to be preferred over a quota. This is important because forcing foreign producers to participate in the EU ETS can be interpreted as a quantitative restriction and is therefore very unlikely to be WTO compatible. In 2009 due to political pressure the attempt to include foreign air travel providers into the ETS failed. If this inclusion of foreign producers/providers would have been subject to the Dispute Settlement Body of the WTO it is very likely that a panel would have deemed it not compatible with WTO rules, especially Article XI. of the GATT.

Full carbon border adjustment

Article XVI. is relevant for the implementation of a full border carbon adjustment. In such a full border carbon adjustment, for every (ton of) product that is exported to countries outside the EU the respective producers would get their costs for buying EUAs refunded or would not have to buy allowances in the first place. This process has to be as transparent as possible in order to not be classified as an export subsidy. It should be noted, however, that the wording of article XVI. is less strict than in other, more important articles, thus making it very likely that a full border carbon adjustment based on article II(2) is WTO-compatible.

Deviation from the general rules of the GATT

Finally, under article XX. of the GATT there is the possibility to argue in front of a WTO panel that a specific BCA design is necessary, even though it violates the MFN, national treatment and/or pacta sunt servanda principle in order to protect human and animal health and life or for the preservation of exhaustible natural resources. Proving this necessity might be possible and it should be mentioned that a WTO panel in US – Gasoline (WT/DS2) ruled that trade restricting policies that protect the natural and exhaustible resource, namely clean, air is permitted under XX(g). However, fulfilling all the requirements of article XX. is not as easy as it might seem because a two-tier analysis is necessary. Once the necessity of a measure (e.g. to protect human life) is established it has to be demonstrated that this measure is not applied in a manner which would constitute “a means of arbitrary or unjustifiable discrimination between countries where the same conditions prevail” and is not “a disguised restriction on international trade”[8]. Regarding this second tier, every BCA design that is not based on article II(2) would face the same difficulties as in complying with article I. and III. of the GATT. In the case that our BCA design based on article II(2) is found to be not compatible with the relevant general rules of the GATT (articles I., II., III., XI. and XVI.) our proposed BTA design will still have the best chances to pass the two tier test of Article XX.

Conclusion

The EU should continue to fight climate change even though unilateral attempts to do so will definitely not succeed in achieving the 2 degrees target. A central element of every successful attempt to curb carbon emissions is to price carbon effectively, which, however, rests on the condition that unilateral climate action will not result in carbon leakage. It is hard to determine empirically whether the EU ETS so far is responsible for either strong or weak carbon leakage. Nevertheless, the current geo-political situation, wherein two of the biggest global emitters are likely to increase their emissions until 2030, and calls within the EU to even step up carbon emission reduction efforts, which would ultimately lead to EUA prices considerably exceeding the current € 25/ton and would simultaneously lead to an even faster decline of the quantity of ‘free’ allowances, should put potential carbon leakage on the top of the agenda of the European Commission.

A central element of every successful attempt to curb carbon emissions is to price carbon effectively, which, however, rests on the condition that unilateral climate action will not result in carbon leakage.

This policy brief’s main focus is to outline a WTO-compatible BCA design, fully aware that the US is currently trying to hamstring the WTO by blocking the appointment of new judges. Wide international acceptance of an EU BCA is nevertheless necessary for the success of this instrument. The proposed design is based on article II(2) of the GATT that allows WTO members to levy a tax (tariff) equivalent to domestic taxes and levies. In order to be able to make use of this article, the EU ETS has to be transformed into a quasi carbon tax. The tax base has to be calculated based on the benchmarks already available in the EU ETS. These benchmarks might need new scrutiny, but they are already product-based and thus applicable for calculating a border carbon tax or tariff. The second requirement is the introduction of a narrow EUA price corridor in order to use the lower bound of this corridor as a non-volatile tax (tariff) rate. This has the additional advantage of creating predictability of the future price path for firms so that they are able to prepare long-term plans and make the necessary (technological) adjustments and investments, thus avoiding lock-in effects.

Wide international acceptance of an EU BCA is nevertheless necessary for the success of this instrument.

It is fully acknowledged that the approach put forward in this policy brief would abandon one of the key features economists cherish the most, namely the incentives for foreign firms/countries to change their production methods. However, every attempt to implement a BCA that discriminates either between importing countries or an importing country and the EU is doomed to fail. The proposed BCA design is likely to be considered compatible with the relevant general rules of the GATT (articles I., II., III., XI. and XVI.) and has in addition the best chances to pass the two tier test of Article XX., which would allow the EU to introduce it irrespective of the BCA’s compatibility with the general rules.

Finally, if a BCA is the measure the EU decides upon to prevent carbon leakage it should aim for a full border carbon adjustment, i.e. exempting EU exports from any form of carbon pricing.

[1] https://www.project-syndicate.org/commentary/european-union-needs-carbon-neutrality-strategy-by-jean-pisani-ferry-2019-07?barrier=accesspaylog

[2] There are in general two channels that lead to carbon leakage as a consequence of unilateral climate action. The first one is the shift of production to countries with less environmental standards. The second channel is the decrease of the world price of oil as a result of less demand inside the EU. This decrease of oil prices could lead to an increase of oil consumption in third countries, thus potentially increasing global emissions.

This second channel, however is less relevant for the topic of this article because EU oil consumption is not as strongly affected by changes within the ETS sectors compared to the non-ETS sectors, such as heating or transport. If heating and transport were to be included in the ETS the issue of carbon leakage would be even bigger.

[3] ‘Strong carbon leakage’ describes the process of existing production moving abroad to countries with fewer environmental regulations, while ‘weak carbon leakage’ describes the process of new investment being made in third countries because of fewer environmental regulations (Davis and Caldeira, 2010).

[4] The MSR is a mechanism that ensures a certain level of liquidity in the EUA market. This means that the current oversupply of allowances will be put into the MSR and will not be available for auctioning. Should the amount of allowances in the market fall below a certain threshold, however, the MSR will release allowances. The MSR, thus, ensures a minimum and a maximum level of liquidity in the market.

[5] See also https://www.wto.org/english/res_e/booksp_e/trade_climate_change_e.pdf, p.100

[6] https://www.wto.org/gatt_docs/English/SULPDF/90840088.pdf

[7] https://www.wto.org/english/res_e/booksp_e/gatt_ai_e/art3_e.pdf, p.137-138

[8] See also: https://www.wto.org/english/res_e/booksp_e/trade_climate_change_e.pdf, p.100

- Aichele, Rahel, and Gabriel Felbermayr. 2015. “Kyoto and carbon leakage: An empirical analysis of the carbon content of bilateral trade.” Review of Economics and Statistics 97 (1): 104-115.

- Böhringer, Christoph, Brita Bye, Taran Faeh, and Knut E. Rosendahl. 2012. “Alternative Designs for Tariffs on Embodied Carbon: A Global Cost-Effectiveness Analysis.” Statistics Norway Discussion Paper (682).

- Becker, Daniel, Magdalena Brzeskot, Wolfgang Peters, and Ulrike Will. 2013. “Grenzausgleichsinstrumente bei unilateralen Klimaschutzmaßnahmen – Eine ökonomische und WTO-rechtliche Analyse.” Zeitschrift für Umweltpolitik und Umweltrecht (ZFU) (Deutscher Fachverlag) 339-369.

- Boyette, Marie. 2018. “CO2-Bepreisung in Frankreich. Europäisches Emissionshandelssystem EU-ETS und CO2-Steuer.” Memo für das deutsch-französische Büro für die Energiewende.

- Bueb, Julien, Lilian Richieri Hanania, and Alice Le Clezio. 2017. “Border Adjustment Mechanisms – Elements for Economic, Legal, and Political Analysis.” In The Political Economy of Clean Energy Transitions, by Douglas Arent, Channing Arndt, Mackay Miller, Finn Tarp and Owen Zinaman, 60-79. Oxford: Oxford University Press.

- Davis, Steven, and Ken Caldeira. 2010. “Consumption-based Accounting of CO” Emissions.” Proceedings of the National Academy of Sciences 107 (12): 5687-5692.

- Dröge, Susanne, Harro von Asselt, Kasturi Das, and Michael Mehling. 2018. “Mobilising Trade Policy for Climate Action under Paris Agreement. Options for the European Union.” SWP Research Paper (Stiftung Wissenschaft und Politik).

- Fouré, Jean, Guimbard Houssein, and Stéphanie Monjon. 2016. “Border Carbon Adjustment and Trade Retaliation: What would be the Cost for the European Union?” Energy Economics 54 (C): 349-362.

- Kemfert, Claudia, Sophie Schmalz, and Nicole Wägner. 2019. “CO”-Bepreisung im Wärme- und Verkehrssektor: Erweiterung des Emissonshandels löst aktuelles Klimaschutzproblem nicht.” DIW Discussion Papers (1818).

- Krenek, Alexander, Mark Sommer, and Margit Schratzenstaller. 2019. “Sustainability-oriented Future EU Funding: A European border carbon adjustment.” WIFO Working Papers (587).

- Monjon, Stéphanie, and Philippe Quirion. 2011. “A Border Adjustment for the EU ETS: Reconciling WTO Rules and Capacity to Tackle Carbon Leakage.” Climate Policy 11 (5): 1212-1225.

- Monjon, Stéphanie, and Philippe Quirion. 2010. “How to design a border adjustment for the European Union Emissions Trading System.” Energy Policy 5199-5207.

- Trachtman, Joel P. 2017. “WTO Law Constraints on Border Tax Adjustment and Tax Credit Mechanisms to Reduce the Competitive Effects of Carbon Taxes.” National Tax Journal 70 (2): 469-494.

ISSN 2305-2635

The views expressed in this publication are those of the author and not necessarily those of the Austrian Society of European Politics or the organisation for which the author is working.

Keywords

border carbon adjustment, WTO, EU Emission Trading System, European Green Deal, EU system of own resources

Citation

Krenek, A. (2020). How to implement a WTO-compatible full border carbon adjustment as an important part of the European Green Deal. Vienna. ÖGfE Policy Brief, 02’2020

{kind=link}